You are currently browsing the category archive for the ‘Competition’ category.

Xi Jinping departed Moscow eight days ago following his three-day state visit. In broad brush, the trip removed some uncertainties about the basic direction of Xi’s positioning on the global stage. No, this was not a peace-broker’s mission. Xi clearly prioritized propping up a faltering “friend without limits” over any serious — or even half-hearted — effort to play the honest broker. Washington and Kyiv still want Xi to talk with Zelensky (likely) or perhaps even visit Kyiv (unlikely) but the aim is not for any mediation by Xi but rather to reinforce the messaging to Xi about not sending lethal armaments to Russia. And, no, Xi seems quite clearly to be prioritizing the recovery of his wobbly economy over the risk of sanctions from the U.S., Europe and key Asian partners should he defy the Biden Administration red-line against China supplying Russia with lethal armaments.

As the third door opens, it’s now possible to glimpse some of the finer brush-strokes of Xi’s long-term plan to counter the liberal, rules-based world order. These are revealed in the 9-point joint statement released by Putin and Xi at the conclusion of Xi’s Moscow visit as well through related moves by China on the world stage. Five of the more subtle brush-strokes to observe:

- Xi used his trip to signal to Washington and to NATO and its other democratic allies that China now largely has Russia under its thumb. It can draw increasingly on Russia as a plentiful supply of heavily-discounted oil and other energy resources. Similarly, it can address its own food insecurity and inflation concerns by throwing its market open to Russian food commodities at cut-rate prices. It can force Russian banks and the Russian financial system to do its bidding (see next point). And it can count on Russia to parrot its propaganda line with particular focus on Africa, South America and the Pacific region. All of this serves to prop up Putin and prolong the war, serving Xi’s interests without triggering retaliation against China.

- Xi revealed that his weapon of choice to counter the post-WWII world order will not be lethal armament deliveries to Moscow but the Chinese yuan (RMB, renminbi). Moreover, he put the brush in Putin’s hand for this particular stroke. Towards the end of the summit, Putin pointedly stated “We (Putin and Xi) are in favor of using the Chinese yuan for settlements between Russia and the countries of Asia, Africa and Latin America.” From a broad strategic perspective, it makes perfect sense that Xi would choose this approach. Why risk retaliation by getting involved in a hot war in Europe (where Russia is losing ground), when China can force Russia to support a Chinese-led challenge to U.S. dollar domination elsewhere throughout the world. The standing of the dollar as the world’s reserve currency is arguably the United States’ most potent, non-military asset globally. Others have tried to dislodge it and have failed. But, as the world’s second largest economy, as the de facto leader of the developing world for the past 50 years, and as a vise-grip political command structure, Xi clearly sees this approach as his best bet for now (while the Taiwan issue still hangs unresolved in the background).

- Putin’s statement comes not as an announcement of any new undertaking by Xi but rather as an exclamation point on an ever-evolving geo-strategic campaign which Xi has been conducting in Asia, Africa and Latin America since 2012 in the form of Belt and Road Initiative (BRI). There is particular urgency to this campaign now in the wake of the COVID pandemic and the recent rapid rise in U.S. interest rates. As a result of these developments, many BRI partner/client countries now find themselves unable to service their earlier loan obligations to China. To adjust, China has been forced to dramatically increase its overall lending through loan restructurings to keep major BRI projects afloat. As a result, Chinese lending to debt-ridden countries now stands at more than $40 billion, not far off the level of the traditional, post-WWII lender of last resort, the International Monetary Fund (IMF), whose loan exposure stands at more than $65 billion. While a strain on PRC finances, this hefty lending posture gives Xi the ability to speak softly (through Putin) while carrying a big stick against the dollar-denominated international order.

- China’s burst of Mid-East diplomacy is a further brush-stroke filling out this picture. The opportunistic stage-craft positioning PRC Foreign Minister Wang Yi as the go-between in the mid-March entente between Saudi Arabia and Iran — which was happening anyhow — was meticulously executed. Likewise, the bullhorn which the Foreign Ministry has used to welcome the possibility of rapprochement between Saudi Arabia and Syria is notable. All of this is leading up to a summit between Iran and the six-nation Gulf Cooperation Council in Beijing in the fall. Against the broad backdrop of events, it is certainly not a coincidence that Mohammed bin Salman, Saudi Arabia’s leader, has been mentioning under his breath the possiblity of settling more of his country’s oil exports with the Chinese yuan.

- A final point is the deep planning behind what is now unfolding. None of this reflects ad hoc or reactive moves in response to the Ukraine crisis. Instead, this plan is organically tied to the development of the ten-year-old Belt and Road Initiative and signs of it became clearer with the convening of the 20th Party Congress last October, with the unveiling of the CCP’s newest Five Year Plan (FYP) and with the announcement of the country’s new ministerial line-up at the Two Sessions meetings in Beijing earlier this month. In hindsight, the strongest proof of this is in the meeting just concluded with Putin. Ukraine was just a minor, slightly discomfiting blip for Xi in Moscow last week, just as it was only a blip for Xi when Putin invaded Ukraine just days after their meeting in Beijing in February 2022 on the eve of the Olympics. Xi is extolled in China as being “unswerving.” At least as far as his plan to offer an alternative world order is concerned, this characterization is apt. No swerving from the plan just because of an unprovoked invasion of a sovereign nation by his Russian friend. As Alexander Korolev’s (University of New South Wales) observed regarding the Xi-Putin 9-point joint statement: “It looks like a strategic plan for a decade or even more. It’s not a knee-jerk reaction to the war in Ukraine.” Fits in well with the three 5-year chapters through which Xi has been telling his heroic ‘rejuvenation of China’ story. A story that can’t end well for Xi without closing the book on Taiwan.

I received an email yesterday from a college friend who is bright, informed and engaged with world events. She is not a China specialist but over the last few years we have had an on-going exchange of views about China, both privately and in a public forum.

Her message from yesterday read,”Terry: Yikes. Do you have access to Le Monde? I can’t read the rest of the article, but the first half is alarming. R.” The article she hyperlinked is from Le Monde and that article in turn hyperlinks to a strategy document which the People’s Republic of China (PRC) has just released in conjunction with the visit by Wang Yi, Xi Jinping’s principal foreign policy advisor, to Munich for the 59th Munich Security Conference with NATO member countries and then on to Russia for meetings with Foreign Minister Sergey Lavrov and yesterday with Putin himself. The document is titled “American hegemony and its dangers.” As headlined — accurately, I might add — in the Le Monde article, the focus of Xi’s Foreign Ministry is now on “‘direct confrontation with the United States.”

Today’s brief post is both my response to her and a way of brushing off the cobwebs after a long holiday vacation — lasting from Thanksgiving through Chinese New Year — I have taken from Assessing China.

To keep it simple, there are two main reasons that this newly overt stance of direct confrontation with the U.S. comes as no surprise from Xi’s PRC in 2023.

The first goes back as far as 1921 with the founding of the Chinese Communist Party (CCP) in Shanghai. Inspired by the Bolsheviks’ gains in the October Revolution, Chen Duxiu and other founding leaders of the CCP made Leninist ideology (soon to become Leninist-Stalinist ideology after Stalin’s rise to power in 1924) the central tent-pole of the party. According to that ideology, the bases of CCP power were the Three P’s — the Party, the PLA (People’s Liberation Army) and propaganda. Since seizing the mainland and ousting Chiang Kaishek’s rival Kuomintang Party in 1949, the centrality of this ideology has only been tested twice. The first was the slow-boil Sino-Soviet split which began in 1956 and culminated in 1972 when China turned its back on its Big Brother in Communist ideology and welcomed Richard Nixon. The second came with the introduction of Deng Xiaoping’s economic reforms which started experimentally in 1978 and were formally adopted in 1982.

The effect of these reforms was monumental. For the first time since 1921, decision-making within the CCP was to be based on a predictable economic logic and not on malleable political ideology. It ushered in a 30-year period of economic growth which according to the World Bank has lifted 800 million people out of poverty. Western observers, myself included, tended to assume that this three decade burst of wealth creation under the post-WWII Pax Americana would be enough to make PRC leadership want to become a permanent “stakeholder” in this global order. In hindsight, we underestimated the strength of the CCP’s ideological ‘muscle memory,’ of its basic political motivation and of China’s civilizational pride (and resentments). What is a seventy-five year Post-WWII order measured against a four thousand year civilizational record in which the Peoples’ Republic of China is, in cultural terms, its latest dynasty. And, as Orville Schell has masterfully made the case in Wealth and Power, not even Deng Xiaoping probably ever saw wealth-creation for China in a Washington-led world order as an end in itself, but rather as a step toward global power that would enable China to challenge that world order in due course. For Xi Jinping, a true ideologue inspired by his father’s revolutionary experience, that time is now.

Secondly, the path that China has been taking to overt confrontation with the West has been revealing itself in planned and increasingly obvious stages ever since 2008. 2008 was the year of the Global Financial Crisis, which China weathered with less turmoil and damage than the advanced economies in the West and Asia. That is the year that CCP leadership started taking stock of what it had gained in capital accumulation and talent acquisition and began thinking about striking out on its own different path. There was still a need to access Western consumer and financial markets and to promote inflow of management expertise along with inbound investment but the critical need was technology. In 2008, China was in no position to compete with the West and Western-aligned countries like Japan, Taiwan and South Korea in advanced technology. For that reason, over the next fifteen years, CCP ambitions were always partially cloaked but increasingly revealed with each Five Year Plan cycle. (See Xi’s Ascension to the CCP Pantheon for a more detailed mapping of that 15-year course). In 2012, the CCP selected Xi Jinping as the horse they would ride on this epochal journey. He would break the mold which Deng Xiaoping had set limiting Chinese leaders to two five-year terms. And he would use his longer leash to bring Hong Kong and Taiwan to heel before stepping down. To usher in the next Five Year cycle of the Politburo in 2017, Xi gave a triumphalist speech telling the world what to expect in the years ahead. Now, fresh from securing an unprecedented third term of formal power last year, Xi is moving to make those stated intentions a reality. The pandemic and Putin’s invasion of Ukraine and Biden’s CHIPS Act were not part of the plan. But Xi and the CCP are ‘unswerving’ in pushing forward with this plan. It has been fifteen years in the making and, for much of it, the U.S. and its allies have been distracted in the Middle East and Ukraine. With its population now in decline, Xi knows the window is closing for him to reshape the global order to his and the CCP’s liking.

With ‘ideology in command’ and riding fifteen years of planning momentum, China’s direction under Xi is now clear for all to see. Xi’s strategic accommodation with junior partner (and client-state energy supplier) Russia last February was simply another way-station on its path. The path to open confrontation with the leaders of the post-WWII order, and the scramble for influence with less tightly aligned global players like Brazil, Hungary, Turkey, South Africa, India and Indonesia, is afoot.

Autocracy vs Democracy. Game on.

The three-hour face-to-face meeting in Bali between President Biden and President Xi — their first non-virtual meeting in over three years — concluded just over an hour ago.

Much can be said (and is already in digital print) looking at this meeting from various angles:

- History of Biden’s personal relationship with Xi

- Composition of the small delegations accompanying the heads of state and what those choices say

- The wide range of issues discussed including Taiwan, Russia, nuclear arms (and their possible use in Ukraine), North Korea, human rights, resumption of national level cooperation on issues of climate change, health security, global food security, and defense-related communications (to forestall accidents and misunderstandings), etc.

- Differences in the official post-meeting read-outs from the two sides and what those differences signify

- Atmospherics of the meeting — effect of recent boosts to each leader’s domestic standing; implications of the third-party location on periphery of G20, etc

But I will go to what I believe to be the heart of the matter. The bottom line, both immediately and over the medium term:

CONTEXT: Gauged charitably, U.S.-China relations are at their lowest point since at least 1991 (post-Tiananmen and pre-Deng’s Tour of the South). Gauged more hard-headedly, they are in their worst shape since before Nixon’s visit to China in 1972 to begin dialogue and explore a relationship amid the Cold War freeze. The vertiginous decline we’ve been experiencing in recent years started very gradually as far back as 2008 when the (Western) Financial Crisis put shortcomings of the Washington Consensus on display in Beijing at the very moment when China was basking in its success in hosting the 2008 Summer Olympics. The hardening of attitudes became personified on the Chinese side with the emergence of Xi Jinping as paramount leader in 2012. Over the following years, the on-going decline in political relations — as contrasted with ever-strengthening commercial ties — became exacerbated for the Obama Administration as China militarized islands in the South and Southeast China Seas, brazenly breaking a commitment Xi had personally given Obama. It was then personified on the U.S. side starting in 2015 with Donald Trump’s racially-tinged campaign and, following his election, by his go-it-alone crusade to punish China with sanctions and Oval Office invective. The rhetoric was answered in 2017 by Xi Jinping upon his re-election as Chinese Communist Party (CCP) head in the form of an uber-triumphalist speech he delivered from the 19th Party Congress stage. The flash-points multiplied during the pandemic with China working hard to obscure the origins of the Covid-19 outbreak and subsequently using its heavy-handed Zero-Covid policy as the linchpin for Xi’s claim that China offered the world a superior system to liberal Western democracy (a claim which non-Western Taiwan makes a mockery of every day and which Hong Kong once also challenged prior to its being brought to heel brutally by Beijing in 2020). The deterioration continued in 2021 as the Biden Administration disappointed Beijing by not reverting to the softer, Obama-era approach to China that the Chinese leadership in Zhongnanhai had expected. Instead, the Biden Administration worked assiduously and with considerable success, to build a broad, values-based partnership with traditional allies and other aligned countries to answer China with a solid front. The Peoples Liberation Army’s practice-run blockade of Taiwan following House Speaker Pelosi’s visit to Taiwan in August further accelerated the downward spiral. And, while not yet fully appreciated by the American public, passage of the Biden Administration’s CHIPS Act into law in August is perceived in China, rightly, as a policy dagger pointed at the heart of its aspirations for seizing dominance in 21st c. technologies for defense, aerospace and space, surveillance and security, and industrial automation and productivity. (It is with the set of issues in these last two sentences — the interlinked issue of Taiwan and the CHIPS Act — that the Assessing China blog is now focused).

THE BOTTOM LINE: The bottom line of today’s meeting is Taiwan. While both sides settled in their separate post-meeting read-outs on emphasizing the lowest common denominator assertion that they’re now working together to stabilize an unstable relationship, their agendas going into the meeting were clearly different. For the Biden Administration, stabilization was the goal. It was enough just to establish a floor to stop further relationship decline and to limit the negative impact further decline would have on the range of issues under discussion (see above). For Xi, the goal was something more — to leverage agreement to stabilize the relationship toward the end of prying out some glimmer of affirmation from the U.S. side to validate his stance on Taiwan. With his eye on 2027 (21st Party Congress) and 2035 (a key CCP goal for China’s development) and with a domestic lock-hold for the next five years in the form of his new Standing Committee of loyalists, Xi is turning his attention — and ambition — to the international sphere. That means Taiwan as the culmination of his China Dream (and, I would wager, the fulfillment of the backroom deal he likely crafted with the CCP in 2012 to let him off the two-term-limit leash). In Xi’s thinking, if the U.S. could commit to the Shanghai Communique in earlier years, he should push as a next step for formal U.S. acceptance of his claim on Taiwan. As Xi put it, Taiwan is “the very core of our core interests.”

The bottom line of their meeting in Bali today may then be that Xi, just like Putin with Ukraine, misreads U.S. politics and society and the resolve of most of the international community concerning Taiwan. The evidence for this view would be the public read-outs: Biden achieved his chief objective while Xi did not.

But another view is possible. As Xi has demonstrated over the last twelve years, he is willing to take large risks to achieve the China Dream but he is methodical about how he goes about taking those risks. Militarization of the South China Sea and the ruthless imposition of the Basic Security Law in Hong Kong are just two examples. Militarily, China has been modernizing and arming up with laser-focus on deterring the U.S. in the Strait of Taiwan for far longer than the Pentagon has been taking steps to respond. As a result, the window of opportunity for Xi to move militarily is expected to be at its widest around 2027 or 2028. Following that, the belated U.S. military revamp in the region will be coming on stream and narrowing that window with each passing year. (It’s worth noting that 2027 coincides with the next Party Congress and therefore coincides well with the ‘chapter structure’ of the narrative Xi has been building about his stature as not only a peer of Mao Zedong in the Communist era but as a Chinese leader of destiny for the ages.)

So does the “failure” of Xi’s bottom-line agenda regarding Taiwan at today’s meeting indicate that he misreads Biden and the U.S. political system? Or might he instead be playing a longer game to a wider audience? If Xi’s sights are indeed firmly fixed on the 2027/8 moment (not only militarily but also politically and in the eyes of history) and if he is focused on exploiting that window of maximum military opportunity, his failure today to make any headway toward some type of formal understanding with the U.S. regarding Taiwan may be exactly the point.

The choreography may be designed to show Xi making a concerted effort to get the U.S. to more fully acknowledge his claim on Taiwan. Xi probably recognizes this won’t happen. The U.S. will not cut a deal with an autocrat to throw 23 million people in a thriving democracy under the bus. But Xi can use that show of effort over the next few years to advantage. He will have made a show for the world to see of having tried hard to exhaust “peaceful measures” prior to being “forced” to make a military move on Taiwan. He will have checked that box. And it won’t be a coincidence if the moment of being “forced” happens at the same moment of the PLA’s maximum military advantage.

After a run of nine years and ten months, the Assessing China blog was blacklisted last weekend in China.

How did it last that long given that my view of the Chinese Communist Party (not the Chinese people) is highly critical? By exercising some diplomatic judiciousness in my posts and by hitching my star to a Presidential-level, bi-national program of U.S.-China clean energy cooperation aimed at mitigating the global effects of climate change at scale and speed. It was in the U.S. interest to cooperate with China on climate change mitigation as long as China was willing to cooperate.

What led to Sunday’s change? Three things …

1. China officially ended all high-level bilateral programs of cooperation with the U.S. — not only on climate change but also, among others, on defense coordination to forestall risks of military miscalculation — in the wake of Nancy Pelosi’s mid-August visit to Taiwan.

2. Last month’s CHIPS Act and last week’s National Security Strategy released by the Biden Administration have raised the salience of work, publications and Congressional Commission testimony I previously did in the 2000s, advocating strengthened trade ties with Taiwan and pointing out vulnerabilities in global semiconductor supply chains

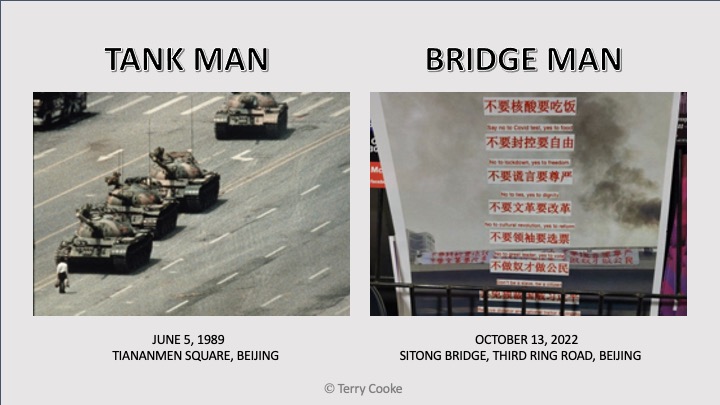

3. In light of 1 and 2, I intentionally courted blacklisting over the weekend by including a link to BBC’s coverage of The Bridge Man protest against Xi Jinping’s and the CCP’s rule in Saturday’s post (which contains the link to the BBC report). The censors didn’t miss a beat in catching this. But, given my shift in focus to Taiwan and microchips, it’s better for me that the blog is now blocked in China and can’t become the focus of netizen ire. I’m just sorry for the subscribers in the mainland who find themselves suddenly cut off.

My wife and I were stationed with the U.S. Consulate in Shanghai at the time of The Tank Man’s protest. That act of defiance as well as this month’s ‘cri du coeur’ by The Bridge Man are extraordinarily courageous acts by individuals against a system dedicated to silencing any voices other than those who choose to be fully obedient or, more frequently, are cowed into full obedience.

by Doug Barry, Senior Director of Communications, U.S.-China Business Council

(view original article in USCBC’s Fifty States, Fifty Stories series)

Policy entrepreneurs are plentiful in America. You can find them everywhere, devoting ideas and energy to getting things done. Terry Cooke founded the non-profit China Partnership of Greater Philadelphia with a focus on getting the United States and China to cooperate on climate change. Getting what he wants done has become more challenging as the two countries ping pong between cooperation, competition, and conflict.

How did he get here and how is he managing multiple challenges simultaneously? He’s been interested in global affairs for a long time, starting in 1988 when he joined the US Commerce Department as a foreign commercial service officer in Shanghai. His two-year posting there bracketed the Tiananmen Square convulsion. Years flew by with postings in Tokyo, Berlin, and Taiwan. In 2002 he took leave from the foreign service and started a consulting business focusing on Taiwan and high tech.

In 2006, Cooke joined the World Economic Forum (WEF) as Director of Asian CEO Partnership with a focus more on Japan than China. He left in 2008. “It was too much travel,” he recalled. “I worked in New York, had my family in Philadelphia, commuted to Geneva, and had responsibility for multiple events in Asia.”

One of the best parts of the WEF job was sitting in on multiple sectoral meetings with CEOs. His main takeaway was that many of these corporate leaders were talking about the challenges of climate change, not as PR or greenwashing, but about the need to transform their companies into low-carbon leaders. “I decided that was the hook that I wanted to hang the second half of my career on when I came back to Philadelphia.”

Cooke recalled his time in Berlin and the impression made by comparing what was then called West Germany with the East, which at the time was terribly polluted. When the Berlin Wall fell, the country united and the cleanup of the Eastern part of the country began. The lesson was that great progress to improve the environment is possible if the political will exists and if clear policy creates predictability for businesses and investors.

The good old days

In 2010, Cooke joined the Wilson Center, a Washington, DC think tank, as senior fellow for US-China climate cooperation. His research there led to publication of his book Sustaining US-China Cooperation in Clean Energy. Coincident with this research, Secretary of Energy Steven Chu introduced a “national labs program for the 21st century” for clean energy technologies as an outgrowth of the 10-year framework for US-China cooperation on energy and the environment pioneered by Treasury Secretary Hank Paulson in the waning years of the George W. Bush administration.

President Barack Obama and Secretary Chu worked to expand Paulson’s program, adding three US-China clean energy research centers in different industrial areas: electric vehicles initially at the University of Michigan, clean coal at the University of West Virginia, and energy efficient buildings through a Penn State-led program at the Philadelphia Navy Yard.

“Disappointing as these decisions were, there was still potential in the climate change mitigation space, even as other areas like micro-electronics drifted further off-limits.”

To support and expand the energy-efficient buildings program, Cooke founded in 2011 the China Partnership of Greater Philadelphia whose mission was raising awareness and facilitating collaboration to create and bring to market low-carbon solutions for the built environment. For the first years, things went great with lots of local and Chinese partners, mayoral visits, and stakeholders to plan low-carbon futures for urban centers in the United States and China. In 2014, China Partnership of Greater Philadelphia and its partner organization in China, the TEDA EcoCenter, were competitively selected for and awarded a prestigious U.S.-China EcoPartnership Award, administered jointly by the U.S. and PRC Governments.

“We had some fits and starts, including an unfortunate near-death experience involving IP piracy.” Isn’t this ironic given the long-standing concerns the US government and private sector have about “collaborations” that lead to forced technology transfers and outright pilfering? “It would be if that’s what happened. Instead, the main culprit was an American in an American company.” The company did not want to make a public fuss because of reputational concerns. “We had to shift focus and change our business model to make sure that would never happen again, but it was a one-off, not something endemic with the work we were doing.”

Pulling the plug on energy cooperation

If not as immediately dire, there were other experiences that could have been crippling to his non-profit. Two of them involved former president Donald Trump, who pulled the United States out of the Paris Climate Accords and in 2020 terminated the US-China EcoPartnership program just seven days before leaving office. “Disappointing as these decisions were, there was still potential in the climate change mitigation space, even as other areas like micro-electronics drifted further off-limits.”

The shifting binaries involved with competition and cooperation were making the scope for business cooperation more limited and the non-profit’s work more problematic. Competition is now spilling into the space previously marked by cooperation. The shriveling of discourse between government leaders has only made things more difficult.

“What used to be very effective work through industrial cooperation in lowering emissions is now off the table, though some academic and some intergovernmental climate cooperation continues.”

Early in the Biden administration, excitement was generated by the appointment of John Kerry as climate envoy. Kerry and his PRC counterpart, Xie Zhenhua, had worked closely and cooperatively under Biden’s vice presidency during the Obama administration but Biden administration policy would not be a simple reset to that period. While cooperation continues in areas such as scientific exchange and standards setting, industrial cooperation toward low-carbon goals now enjoys little federal-level support. This even as the planet continues to warm and nations like China and India continue to struggle reducing their addiction to coal.

Kerry recently pointed out in a Foreign Affairs article that there’s still time to avoid disaster but that in the coming years many trillions of dollars will be needed to fund and field clean energy technology. The money, he said, must largely come from the private sector which stands to gain from what could amount to a new industrial revolution.

Cooke worries that the emphasis on zero-sum competition with China over recent years will make broad cooperation in climate change extremely difficult. “The competition drive is spilling into areas that used to be defined by cooperation,” he said. One example is the network of 11 national-level eco parks organized through the Greater Philadelphia-Tianjin EcoPartnership. Germany invested in one such park in 2020, focused on green maritime technology, to the tune of more than $3 billion. The PHL-TJ EcoPartnership had defined a focus on energy-efficient, securely smart and healthy buildings at sustainable-city scale for this network of 11 eco-parks. The emphasis was on large-scale opportunities supported by very large companies and leavened by the innovation of smaller, entrepreneurial companies. “Given the problems in the bilateral relationship, that large scale opportunity has receded for the foreseeable future at least.”

Enter the contradiction

Cooke is highly attuned to the potential for contradiction between commercial competition and climate cooperation, worrying that when Kerry steps down, the space for commercially led environmental solutions to be applied at scale and speed in the two largest global economies will shrink even more.

“What used to be very effective work through industrial cooperation in lowering emissions is now off the table, though some academic and some intergovernmental climate cooperation continues.” He concedes that the continuation of even these relationships is not assured given the political environment in both countries.

“My organization was about creating a platform for a US-Sino Eco-Park in China bringing advanced energy efficiency services and technologies to the park. That is viewed negatively now in Washington. What’s disappointing is that other countries friendly to us are now established in China in commercial areas that we’re better at but won’t be able to contribute to because official reluctance for cooperation.”

Cooke says: “The United States needs to be smart about its clean energy approach to China. Yes, China wants to dominate an emerging 21st century industry. But if we out-innovate and out-compete China technologically, we can access their market profitably and also collaborate commercially to forestall the worst effects of climate change. Is it really in the US interest not to have active engagement with China, aside from discrete small companies that are more easily taken advantage of? I’d prefer to see us going in with a convoy approach of large companies and smaller innovators protected by US government policies and focused on delivering measurable, low-carbon solutions at a globally impactful scale. To my mind, this is a huge missed opportunity.”

Cooke’s non-profit, which he recently rebranded as ReGen250 to accommodate additional, non-China-focused environmental programs, continues to assess options for low-carbon partnerships with China. What elements would a US private sector partner want to support that his organization could strongly endorse? “Alternatively, we can just decide we’re only going to focus on local programs in the Mid-Atlantic to increase access to a greener built environment.”

What about the Department of Energy’s prior interest in cooperation? “I have had some high-level discussions within the Department. The entire group that previously supported the commercial exchange at this high level between the national government and subnational actors, including Eco-Partners and city level groups, is not active right now. It was disappointing to learn that.”

“Despite the challenges in the US-China relationship, subnational initiatives, especially in energy and climate change mitigation solutions, should be encouraged and supported.”

Despite the setbacks, Cooke believes there are still areas for engagement with China regardless of the government in power. One involves people-to-people exchanges, albeit challenging at the present moment given China’s zero-COVID policies. Examples of programs that deserve to survive are the adoption of Chinese children, music (he helped the Philadelphia Orchestra create an artist residency program in China) and artistic exchange, student exchange, and most importantly, business. He believes that the once promising universe of business cooperation has constricted but there still remain spaces outside of sensitive technologies where businesses can and must connect.

As a member of the local ecosystem that support US-China commercial relations, he’s not giving up. Rather, he envisions the different China business-related ecosystems across the United States networking and sharing best practices. He said that one such effort was made recently at a Midwest university, but he expressed some disappointment at the fact that the focus turned out to be on a recently discovered vulnerability involving WeChat. It was a security-led briefing, not the commercially minded dialogue that is needed.

Cooke isn’t ready to walk away from his gift of multi-stakeholder cooperation on climate change or the imperative for non-profits like his to act locally and globally. “Efforts at the subnational level have an important place in helping American companies navigate a complex environment in China. They have a great potential impact because they can organize a well-protected convoy in the place of one isolated boat, big or small.”

“Despite the challenges in the US-China relationship, subnational initiatives, especially in energy and climate change mitigation solutions, should be encouraged and supported.”

(view original article in USCBC’s Fifty States, Fifty Stories series)

After a puzzling on-again, off-again trade action against China’s information and communications technology (ICT) giant ZTE in 2018, the Trump Administration began sanctioning China’s number #1 ICT player Huawei in May 2019. The sanctioning action involved putting Huawei on a Commerce Department “entity list” and thereby restricting U.S. suppliers from selling their goods and technology to Huawei.

As with all of Trump’s trade actions against China, impulse outweighed well thought-out execution in the Huawei crackdown. Initially, some sales were allowed and others denied without clear criteria being communicated to U.S. industry. Later, without preparatory signaling, the Huawei campaign was intensified by expanding U.S. government authority to require licenses for sales of semiconductors made abroad with American technology.

The fitfulness of this policy can be measured by (1) the number of licenses (and dollar value of affected goods and technology) pending but held up in the inter-agency process and (2) the number of licenses (and dollar value of affected goods and technology) which had been applied for by U.S. companies but not processed towards the end of the Trump Administration. (As things stood at the time of the November 3rd election, the expectation was that products in both categories which had clear 5G application would likely be rejected while non-5G products would likely be processed on case-by-case basis.)

Meanwhile, in the international sphere, the Trump Administration pursued a parallel campaign to try to persuade traditional allies to disallow Huawei technology from 5G infrastructural build-out in their respective markets on the grounds that – despite price and performance competitiveness — Huawei’s products represent a national security threat. The results of this international campaign were mixed at best, not least because many of these traditional allies had themselves been targets of different tariff sanctions under Trump’s America First trade policy. Without delving into the changing fortunes of this campaign at different times in different parts of the world, a summary headline on November 3rd might have read “Trump’s 5G Campaign Against Huawei: Embraced in India, Accommodated in the UK, Begrudged in Germany and Repudiated in Thailand and Elsewhere.”

The Biden Administration, while making a quick and clean break from Trump Administration trade policy in the area of climate change mitigation and clean energy technology, has largely kept the Trump Administration domestic policy of restrictive licensing for sales of advanced ICT goods in place. At least, it has made clear that no substantive change should be expected until after the completion of a whole-of-government review of China trade policy and a parallel review of strategic global supply chains which includes semiconductors. In the international arena, it has relaxed the narrowly-focused pressure campaign against Huawei adoption in favor of a more broadly-conceived alliance strategy to rally traditional allies and other democracies to rise to the 21st century challenge posed by China’s autocratic model.

So where do things stand today? The restriction of supplies of U.S. advanced semiconductors to Huawei under both the Trump and Biden Administrations has taken the biggest toll on Huawei. Less impactful but still a headwind for Huawei has been the doubt sown internationally as the U.S. and China edge closer towards global confrontation and supply chain de-coupling. The result? Huawei reported last Friday its third straight quarterly decline in revenues, falling a significant 38% against 2021Q1 results.

Huawei is likely to remain at the center of a highly-fraught tug-of-war between the U.S. and China over 5G. On one side, China has ability to leverage the world’s largest installed base of advanced mobile phone users in the world. On the other, the U.S. dominates the global market for the advanced microchip designs on which advanced telecom markets depend. And the U.S. maintains close partnerships with the world’s leading microchip fabricators in Taiwan and the makers of the world’s leading fabrication equipment in the Netherlands and elsewhere.

Expect more tremors and seismic activity on this fault-line for the foreseeable future. Just last week, the PRC government issued retaliatory actions against Huawei’s main Western rivals – Sweden’s Ericsson AB and Finland’s Nokia, among others. And, as fall-out from the recent spread of the SARS-COV-2 Delta-variant in China, it was announced over the weekend that the World 5G Conference – scheduled for August 6-8 in Beijing – would be postponed indefinitely. Pressure continues to mount while chances to release that pent-up pressure close off.

“We are in competition with China and other countries to win the 21st century,” Biden said on April 28th. “We are at a great inflection point in history. We have to do more than just build back better. … We have to compete more strenuously.”

The question we are examining today is what does “compete more strenuously mean.” I’ll be identifying four distinct fields in which heightened competition is likely to come to the fore but first some context and disclaimers.

The first point to note is that, in President Biden’s own words, some partial answers are already clear. Biden has made clear that he sees this 21st century competition as one between the US and its democratic allies on the one side versus Xi, Putin and other autocratic leaders on the other side. in other words, the heart of the competition is democracy versus autocracy. What Biden has also made clear involves timing, that the competition will not be joined in earnest until the U.S. has emerged from the worst of the COVID-19 pandemic and largely revitalized the performance of the U.S. domestic economy.

Two caveats are also in order. The analysis provided below is strictly my own. The Biden administration – under Kurt Campbell, deputy assistant to the President and coordinator for Indo-Pacific Affairs at the National Security Council — is currently directing an assessment under which cabinet-level departments and some agencies are re-viewing their policies and procedures as they relate to China. These departments and agencies will be reporting their findings to the White House later this year at which point Kurt Campell, his senior director for China Laura Rosenberger, and their staff will be synthesizing these inputs and articulating an updated “whole of government” policy towards China. (This process is consistent with the ‘get our house in order now’ before focusing on generational competition with China, as referenced above.) Clear answers to the question we’re examining today likely won’t be rolled out by the Administration until that process is complete.

In the meantime, the single best open-source for a quasi-authoritative readout of Biden’s thinking on what heightened US- China technology competition will look like may be the Penn Biden Center. While I am affiliated with Fox Leadership International under the School of Arts and Sciences at Penn, I want to make clear that this blog post does not draw on any information from that source. This is my analysis and I bear sole responsibility for any deficiencies.

So, on to the substance …

At the broadest level, the U.S. needs to up its game in four areas of traditional strength to respond more effectively to the 21st century tech challenge from China:

Field 1: Industry Sector Focus

NASA’s manned mission to the moon and DARPA’s role in the creation of the internet are the most storied examples of U.S. Government success in mid-wiving new high technology industries. What has changed since those early post-war successes is the subsequently accelerated pace of technology innovation and development in the Fourth Industrial Age. In fields as diverse as semiconductor design and fabrication, 5G telecommunications, artificial intelligence and robotics, quantum computing, EV batteries and biotechnology, U.S. government policy is currently nowhere near as focused in positioning its support role as is China. What is called for is not a return to 20th century “industrial policy” (and its poor record of picking company-level winners and losers) but a new, 21st century approach to policy support to better prepare eco-system support for the emergence of entire new industries.

Field 2: Funding for Innovation & Regulation of Foreign Acquisitions

Despite the recent trend-line of falling investment in basic research in the U.S. and increasing levels of basic research investment in China, the fact remains that China is still no match for the U.S. in terms of the breadth, depth and quality of its basic research or of the commercial potential of the developments it spins off. This is readily apparent in cutting-edge fields like advanced semiconductor design and gene therapy. In these fields, China can’t put a home-grown team onto the field but instead tries to snap up foreign talent and fledgling foreign companies in hit-or-miss hopes of leveraging that into a domestic breakthrough. Committee on Foreign Investment in the U.S. (CFIUS) and other related government entities need more focus on the dynamics underpinning tomorrow’s industries and less on yesterday’s. Likewise, less silo-ing between basic research and commercial development is urgently needed.

Level 3: Rule of Law

Perhaps no societal field offers greater contrast between the U.S. and China than the field of law and legal practice. The U.S. system of case law based on precedent stretches back to the time of the Saxon Kings of England (with very occasional admixtures from the Roman system of law more common to Continental Europe). As enshrined in the U.S. constitution, ours is the rule of law, not the rule of men (or women). While the Chinese Communist Party (CCP) has borrowed legal ‘parts’ from a wide variety of sources since 1949, the legal system it has assembled from those parts is principally designed to serve the interests of the governing party rather than to protect inherent rights of its citizens or its private companies. It is rule by law, rather than rule of law, as was vividly demonstrated with the imposition of the new security law in Hong Kong in the summer of 2020. Despite the slowness and costs associated with it, the U.S. legal system provides a level of predictability and protection for investors and businesspeople which can’t be matched in China. We can expect to see the Biden Administration act to shore up the foundations of this legal system following the strains put on it by the previous administration.

Level 4: Wellsprings of Economic Vitality

Two of the deepest sources of support and revitalization for technology innovation in the U.S. are immigration and our capital markets. Immigration brings a steady stream not only of young and eager workers but also on occasion transformational business talent such as Sergey Brin and Elon Musk. Our capital markets spread risk over a broad pool of investors and investment vehicles, incentivize iconoclastic thinking and efficiently channel capital to the points of likely greatest return. While China has through its tax policy been impressively building an investment-led structure for its markets, the efficiency and speed of execution of the U.S. capital markets can’t be matched in China. In broad view, China currently tries to leverage its centralized leadership and ‘command economy’ model to try to neutralize this U.S. advantage as well as hoping to ride the momentum from its high-growth domestic macro-development over the last four decades (and the internationalization of that development model over the last ten years). How China fares in field of competition in the years ahead as it emerges from its fast-growth phase of development and collides with a dire demographic imbalance will be one of the more consequential questions of the early 21st century.

Editorial Note: Upcoming posts in the TEA Collaboratives T-series on technology topics will pick up and expand on some of the topics identified above. Our focus in this Technology Competition sub-series will mostly fall under the industry and innovation topics identified above but we will also have occasional invited guest experts to delve more deeplly the legal and capital markets topics. Also, it’s important to note explicitly that the viewpoint expressed in this post and other future posts in the series are obviously a perspective from the U.S.-side. We will present the ‘emic’ view (as seen through the eyes of Chinese government planners and officials) separately through our A-series (Ambitions) posts which appear on Fridays.

As a final note, the Technology Competition sub-series posts introduced in today’s post will alternate on Mondays with our TECH-tonics sub-series posts (which focuses exclusively on issues associated with the micro-electronic supply chain fault-line between the U.S. and China passing through Taiwan). In any given month, we’ll be producing in alternating fashion two posts in the TECHtonics and and two poss in the Tech Competition sub-series.

On May 27th speaking at the annual Stanford University Oksenberg Conference, Kurt Campbell, Biden’s National Security Council Coordinator for Indo-Pacific Affairs, delineated the new ‘continental divide’ in U.S.-China Relations.

The period in U.S. policy toward China that was broadly described as ‘engagement’ has come to an end, said Dr. Kurt M. Campbell, deputy assistant to the President and coordinator for Indo-Pacific affairs at the National Security Council, speaking at Shorenstein APARC’s 2021 Oksenberg Conference. “The dominant paradigm is going to be competition. Our goal is to make that a stable, peaceful competition that brings out the best of us,” he added.

This low-key pronouncement is attention-grabbing for several fundamental reasons: (1) it marks the end of a 39-year bipartisan effort to encourage China to become, through a concerted program of cooperative outreach, a “responsible stakeholder” in the post-WWII liberal democratic world order and (2) the epitapth was delivered by one of the principal architects of that cooperative program.

To back up this somewhat sweeping statement on my part, I’ll be spending the weeks ahead examining what this sea-change portends from three perspectives:

Aspirationally …

On Mondays, we’ll be looking at various aspects of what heightened competition with China will look like for the Biden Administration in the tech sphere. This will include high-level perspectives of competition in artificial intelligence and robotics; sourcing of rare earths needed for smart phones, electric vehicles and other high-tech products; 5G build-out in domestic and international markets; quantum computing competition; the Great Firewall of China as an export product to Belt & Road partners countries; and social media platforms and data privacy issues. But most saliently, we’ll be looking in-depth at global supply chains in microelectronics and the fraught issue that 40% of the world’s microchip production — and 80% of its high-performance products — are produced in Taiwan at a distance of only 90 miles from the PRC mainland.

On Wednesdays, we’ll be examining the fields of energy and environment where cooperation still rules the day under Cabinet-level John Kerry’s aegis but where cooperation is shifting from a government-to-government level to a more market-based model of comparative advantage cooperation.

On Fridays, we’ll be examining what these changes look like from the Chinese perspective. Our sources for this perspective — what cultural anthropologists call the emic (in-group) view as opposed to the etic (outside observer) view — will include macro-perspectives such as the Five Year Plans, primary-source research findings provided by my UPenn masters-level students, and also micro-perspectives such as interviews and insights gleaned from business people operating on the ground in China.

My heart-felt thanks go out to the many subscribers who have been with me on the journey to date. I look forward to welcoming hopefully many others choosing to subscribe to the blog for this next leg of the journey.

Volume 2, Number 4 in Global TECHtonics: U.S./China Fault-line series

The weekend’s big development in the technology arena is Beijing’s eleventh-hour move to alter the timing and trajectory of the sale of TikTok’s U.S. operation.

We touched on the Trump Administration’s August moves against TikTok’s parent Bytedance in the U.S./China De-Coupling: 4 Levels of Risk post two weeks ago. On August 6th, President Trump signed two executive orders which started a 45-day time-clock involving two Chinese companies with hugely popular social media apps – ByteDance (owner of TikTok) and Tencent (owner of WeChat). According to those orders, U.S. citizens and businesses would be barred, once the 45-day period expired, from any transaction involving the company and/or its products. On August 14th, the Trump Administration modified the order as far as it affected TikTok by putting a new order in place, giving TikTok 90-days within which to complete the divestiture of its U.S. operation to an approved U.S. corporate buyer.

The widely-presumed reason for this change being made so shortly after the announcement of the original order is that U.S. potential buyers interested in acquiring the U.S. operations of TikTok had pitched their interest to the White House. It is not surprising that U.S. potential acquirers would be focused on TikTok and not WeChat. The number of TikTok users in the U.S. is estimated at 80 million in comparison with 19 million for WeChat. Its growth rate in global markets is far faster and, critically, its algorithms have nearly ubiquitous applicability whereas WeChat algorithms are more geared to Chinese user behavior and are so less replicable in other world markets.

Two groups of interested buyers have emerged publicly since the August 14th announcement:

- Microsoft/Walmart: As Instagram and other social networks edge into offering shopping features, Microsoft and Walmart are looking to establish themselves at the strategic center of this opportunity with one bold acquisition move. Put simply, Walmart would provide the e-commerce component for TikTok while Microsoft would manage the crucial cloud-computing infrastructure. The deal offers competitive advantages to both firms – Walmart would become better positioned to compete with Amazon and Microsoft would gain experience with an innovative and cutting-edge set of algorithms and data-sets.

- Oracle: According to analysis by the New York Times business reporter Mike Isaac, “Oracle could use TikTok’s data about social interactions to benefit its cloud, data and advertising businesses.” Also, like Microsoft and Walmart, Oracle is interested in the opportunity the deal would afford “to offer customers a hyper-personalized experience in both content and commerce.”

Going into the weekend, the expectation was high that Bytedance’s preferred acquisition partner would become known and that negotiations would shift to a new phase of negotiation with only that chosen partner.

So, what was the development over the weekend which changed the trajectory and pace of this deal? The Chinese government announced late in the day on Friday that any sale of Bytedance’s assets would be subject to a brand-new set of restrictions affecting artificial intelligence exports. As reported in still-developing coverage in the Wall Street Journal, “the new Chinese restrictions highlight the extent to which TikTok, a breakout social-media hit—especially with younger U.S. users—has been thrust into a geopolitical contest between the U.S. and China over the future of global technology.”

I’ll limit my commentary on this development to three main points – a historical observation, a key point having to do with the present-day competition in advanced technologies between the U.S. and China, and my personal handicapping of where this deal is likely to go in the weeks ahead.

Historical Antecedent: The U.S.-Japan Trade War

While observers sometimes invoke the U.S.-Japan Trade War as a template for understanding our current tensions with China, the contrasts between the two are probably more instructive than the similarities. A future post will return to the broad comparison. For our purposes here, I will single out one important point of contrast. The U.S.-Japan Trade war became incandescently hot as a political issue in the lead-up to the 1992 U.S. Presidential election. But while that was happening, commercial developments on the ground were already in motion to begin lowering the heat. The industry sector in which the grass-roots transformation took root and started having great effect was the automotive sector. The seed for that bottom-up transformation was the fact that, post-war, Japan had developed intellectual property in their domestic market that made them more competitive than the U.S. industry in a number of vital areas of automotive manufacturing (e.g., inventory management, quality control, customer-based innovation, etc). Led by Toyota, the Japanese and U.S. industries started reaching an accommodation even before politicians in the U.S. turned up the volume on their anti-Japan megaphones. Japan would license out its intellectual property and bring its production closer to its customers in the U.S. by building factories and supplier networks in the U.S. In return, American companies would gain access to know-how in areas where its competitiveness was lagging and also gained greater access to the restricted Japanese market. At a political level, investments in new state-of-the-art production facilities in the non-unionized south brought jobs into key congressional districts. Of equal importance, auto workers, their families and their communities started having the experience of working alongside Japanese managers on U.S. soil. In the process, real-world people-to-people experiences built on collaboration replaced the one-dimensional caricatures being amplified by politicians and the media.

The Chinese have studied this experience whereby Japan lessened the political tension of the U.S.-Japan Trade War while, simultaneously expanding access to the lucrative U.S. market and affluent U.S. consumers. For various reasons, they have not been as successful in applying the model. We’ll examine the broader set of reasons in a future post but, for present purposes, one salient reason is that China, generally speaking, has not developed the portfolio of intellectual property focused in high-value industries (like, for Japan, automotive and consumer electronics) and highly sought after by U.S. companies. Except, that is, until now as China emerges with competitiveness in advanced technology fields such as artificial intelligence, robotics, and autonomous vehicles.

Looking at Both Sides Now:

The U.S. innovation ecosystem represented by Silicon Valley is, and is likely to remain for the foreseeable future, peerless in many important respects – depth of talent and experience, access to capital, connectivity to leading universities, basic research capability and innovation mindedness. In three respects, however, emerging tech competitors in China enjoy advantages which U.S. firms can’t match. First, China has been for years the biggest and fastest growing market in the world and U.S. companies can’t afford to cede that base of users entirely to their Chinese competition to monopolize. However, the ability of U.S. firms to access those consumers is highly constrained by a whole raft of protections – many non-WTO compliant and others not yet covered by WTO ground-rules — by which the Chinese government limits foreign access to its home market and by which it supports its home-grown champion companies. Second, China may enjoy a tactical advantage through its laser-focus on market applications (as opposed to research and academically-based innovation). Third, AI firms in China definitely enjoy a leg-up in algorithm development because they have direct access to the world’s largest user-base for smart phones and are less constrained by privacy protections for those users. These latter two advantages for Chinese tech firms are persuasively presented by the former President of Google China, Kaifu Lee (a Taiwanese national whose computer science PhD thesis at Carnegie Mellon gave birth to the world’s first speaker-independent, continuous speech recognition system) in his book AI Superpowers: China, Silicon Valley and the New World Order. In Lee’s view, “the United States may have been a first mover in AI but that advantage will not last forever. The AI era will reward the quantity of solid AI engineers over the quality of elite researchers. Strength will come from an army of well-trained engineers and entrepreneurs, and China is training just such an army.”

So, stepping back, there is now for the first time since normalization of U.S.-China relations a strategically-important (emerging) industry where Chinese firms hold important competititve advantages over the U.S. Unlike democratic Japan, this high-stakes competition is associated with a Communist regime with all that that entails for public attitudes in the U.S. And there is little in the of way local ties-that-bind being built quickly and effectively on a people-to-people basis. Nothing that can match the stabilizing experience with Japan investment into the U.S. in the 1990s. Together, these three factors go a long way to illuminating the huge pressures that have been building up under the U.S./China technology faultline on both sides of the U.S. political aisle.

Where’s The TikTok Deal Likely to Go?

Despite the fact that practically nothing is known yet about the details of the PRC government restrictions announced on Friday, two things can be safely said. First, the fact that the PRC government is invoking national security as a basis for governing the commercial activities of its leading artificial intelligence firms is hardly surprising. The competition between the U.S. and China is, for reasons just examined, acute. The U.S. and other countries routinely monitor and manage international commercial activity for their technologically-advanced products and services, especially those that are ‘dual-use’ in both commercial and military applications. The second point is that the timing of the announcement tends to be viewed in the U.S. as so transparently tied to the on-going negotiation involving TikTok that it will be viewed more as a political beanball, than a fair pitch. This despite the fact, as pointed out by an astute comment (see below), that these new regulations had been proposed prior to Trump’s August 6th announcement and were in a public comment process.

The Chinese government action raises the prospect that key algorithms and other vital data – everything that makes TikTok tick — may be stripped out of the sale by its Chinese parent corporation as a new requirement of Chinese law. That result would fundamentally change the value proposition for both the Microsoft/Walmart and Oracle bidding teams. It’s like the difference in value between a top-of-the-line computer and that same computer with all its electronics removed. At the very least, the PRC government action will force all parties to slow the pace of their negotiations and delay the deal being sealed until there’s greater clarity about what will ultimately be allowed.

With Friday’s move, it’s likely that the Chinese government will be satisfied with slowing the deal and changing the trajectory of its fall-out for global technology competition. Scuppering the deal entirely would risk dramatically escalating the issue with Trump and his Administration. That would go against China’s temporary strategy of muted response to the Trump Administration’s recent, pre-election flurry of jabs. The idea in Zhongnanhai in the run-up to November 3rd is to give its wolf-warriors and nationalistic netizens enough to appease their appetites but not enough to risk fanning Washington-Beijing flames out of control.

So, with the clock ticking down to 64 days before the U.S. election and with 78 days before the Trump Executive Order 90-day deadline expires on November 12th, the endgame of this global chess match is now ruled by the time-clock.

TikTok, TikTok, TikTok …

Volume 2, Number 3 in Global TECHtonics: U.S./China Fault-line series

A U.S.-led initiative to reach out to China and to welcome it into the community of Western nations began with President Nixon trip to Beijing in February 1972. Orchestrated by Henry Kissinger, Nixon’s National Security Advisor at the time, the trip was a brilliant Cold War gambit to exploit the growing rift between Moscow and Beijing. The trip kicked off a seven-year process of “normalizing” relations between the West and “the sleeping dragon” of Asia and, in so doing, divided the Soviet bloc. Through almost half-a-century and a bipartisan succession of Presidents, the effort to engage with China continued as that country woke from its Cultural Revolution nightmare and began to rise up, shaking the world as it did so.

February 1972 was the Year of the Rat (Water Element) in the Chinese zodiac. Forty-eight years later we are again in the Year of the Rat under the Metal Element. In Chinese traditional thinking, we have gone from a time of suppleness and fluidity to a time of hardness and intransigence. In the minds of most Western observers, we have passed from a strategic engagement with China to, under President Trump, a time of open competition on the world stage and strategic disengagement (“de-coupling”) in the technology arena.

This post will save for another time the broader discussion about how and why this shift came about other than to make three general, even obvious, points. First, there was undoubtedly a measure of optimistic naïveté in the West in assuming China’s willingness to dutifully assume the role of a ‘responsible stakeholder’ in the post-WWII world order. If the Chinese had conceived of their nation as only having been born in 1949, assuming the mantle of responsible Pax Americana stakeholder might have fit more comfortably. As it was, Chinese conceived the People’s Republic of China as the heir to a Chinese polity which had been the dominant economy in the world for sixteen of the previous eighteen centuries. They weren’t predisposed to simply adopting some newcomer’s rules and norms as to how China should conduct itself on the world stage. Second, there has undoubtedly been tactical overreach and ill-advised swaggering by President Xi Jinping since his triumphalist speech at the 19th Party Congress in September 2017. U.S.-China relations would undoubtedly be on a more stable track today had Xi Jinping played his cards differently, following suit more with Deng Xiaoping’s opening bid of “keeping a low profile (hiding one’s capacity) and biding one’s time” (韜光養晦、有所作為) rather than flashing his Made in China 2025 card so conspicuously. It can be argued that it’s better from the U.S. standpoint for this “world order competition” to be out in the open. Third, the horse is definitely out of the barn. No U.S. Administration is going to try to get that horse back on the 1972-2017 normalization track. The world has changed and what is needed is a U.S. Administration which recognizes real challenges from China but does not exaggerate them and which marshals the resources to address those challenges in an efficient and effective way, rather than wastefully and non-productively.

The remainder of this post uses last week’s The Four Levels of Risk post as a backdrop to a quick sketch outlining just how wasteful and ineffective the Trump Administration’s policy of technology de-coupling from China is becoming. I’ll do this sketch with three brushstrokes – the view from U.S. boardrooms, the view from the cultural sidelines and the view from history.

The View from U.S. Boardrooms

A CNBC.com article by Arjun Kharpal published on June 4, 2019 made no reference to the Tiananmen anniversary but did point out that the Trump Administration’s Huawei policy was quickly hoisted on its own petard – failing to get allies to broaden the campaign but leading to a marked acceleration of China’s efforts to develop its own semiconductor industry to supplant U.S. semiconductor supply in the Chinese market and, eventually, in world markets. “The Huawei incident has indeed stimulated the development of China’s domestic chip industry,” Gu Wenjun, analyst at China-based semiconductor research firm ICWise, told CNBC by email” wrote Kharpal at the time. Now, one year later, Trump Administration policy is digging this hole deeper and at a faster pace:

A CNBC.com article by Arjun Kharpal published on June 4, 2019 made no reference to the Tiananmen anniversary but did point out that the Trump Administration’s Huawei policy was quickly hoisted on its own petard – failing to get allies to broaden the campaign but leading to a marked acceleration of China’s efforts to develop its own semiconductor industry to supplant U.S. semiconductor supply in the Chinese market and, eventually, in world markets. “The Huawei incident has indeed stimulated the development of China’s domestic chip industry,” Gu Wenjun, analyst at China-based semiconductor research firm ICWise, told CNBC by email” wrote Kharpal at the time. Now, one year later, Trump Administration policy is digging this hole deeper and at a faster pace:

- Qualcomm is reported to have lost current orders worth as much as $8 billion as a result of the Trump Administration’s May 2020 tightening of trade restrictions imposed against Huawei. The new regulations block all chipmakers that use U.S.-made equipment or software from producing chips for Huawei (though companies can apply for a license to continue supply)

- Following the Trump Administration’s August 6th signing of an Executive Order banning transactions by U.S. companies with Tencent, the owner of the WeChat app, market research firms scrambled to assess the impact on Apple and its installed base of iPhones in the strategically vital Chinese market. The surveys all pointed to the same result – as many as 90% of iPhone users in China would drop the Apple product and switch to Android devices if the WeChat app were no longer available on their iPhones.

- The same August 6th Executive Order targeted Bytedance, parent company to the massively popular TikTok app. Seasoned observers who are able to gauge the U.S.-side push-back against this action and know the sloppiness with which the Executive Order was drafted, expect an eventual climbdown by the Administration – if not before the November 3rd election, then shortly after it.

The View from the Cultural Sidelines

There are two culture wars raging – a partisan one in U.S. domestic politics and an international one between a suddenly tarnished U.S. model and a much-hyped “bright and shiny” new Chinese model. The same dynamics at play with the COVID-19 pandemic are at play in the technology sphere. Domestically, Trump works to energize his base with claims that China is the enemy and that his Administration’s COVID response and China de-coupling response are “the best” that any President could possibly do. Front-line health workers and tech experts know that, in both cases, the claim lies far afield from the truth.

There are two culture wars raging – a partisan one in U.S. domestic politics and an international one between a suddenly tarnished U.S. model and a much-hyped “bright and shiny” new Chinese model. The same dynamics at play with the COVID-19 pandemic are at play in the technology sphere. Domestically, Trump works to energize his base with claims that China is the enemy and that his Administration’s COVID response and China de-coupling response are “the best” that any President could possibly do. Front-line health workers and tech experts know that, in both cases, the claim lies far afield from the truth.

In China, the popular view cuts to the bone of Trump Administration posturing. His new nickname is 建国 (Jiànguó), a popular name given by parents to their infants especially during the nationalistic years of the Cultural Revolution. It means “Build the Country.” In other words, Trump Administration policies are widely seen as accelerating the same nationalistically-driven Sputnik-type race to advanced semiconductors, artificial intelligence, robotics and the tech future which the policies ostensibly are meant to forestall. Trump’s impulsive “Only I Can Fix It” approach playing to a grandstand of partisan supporters has made the challenge which Xi Jinping’s China presents the U.S. more acute. An approach which takes measured and deliberate stock of that challenge and which aligns interests and works closely with the U.S. business community and international partners would be far more effective. Pumping up nationalist sentiment in both the U.S. and China serves only to narrow options and increase risks of conflict spiraling.

The View from History

A pithy take on Trump’s approach to the U.S.-China technology challenge comes from a widely-respected former colleague who has decades of high-level experience with China from political, national security, economic and think-tank perspectives. He writes “(Trump is like) King Canute trying to fight, instead of the ocean tides, the tides of technology.”

A pithy take on Trump’s approach to the U.S.-China technology challenge comes from a widely-respected former colleague who has decades of high-level experience with China from political, national security, economic and think-tank perspectives. He writes “(Trump is like) King Canute trying to fight, instead of the ocean tides, the tides of technology.”

I’ll conclude with another, somewhat longer historical reference which illuminates Trump’s campaign of China-bashing as a central element of his re-election strategy. It is drawn (almost) verbatim from Episode 66 of The History of Rome podcast series by Mike Duncan:

“Conscious that his standing with the people was taking a hit, the Emperor decided he needed to find someone to take the fall for the fire. Someone he could point to and say it was them, not me, I didn’t have anything to do with it. But he couldn’t just grab someone off the street because, with his popularity sinking like a stone, that would just engender the further charge that he was setting up some innocent to take all the blame. What Nero needed was someone, some group that the people disliked even more than him, someone that the people were ready, willing and able to believe had done this horrible thing if for no other reason than that the people were looking for an excuse to round up and punish them. Enter the Christians. In the thirty odd years since the death of Christ, nascent Christian communities had begun cropping up throughout the Empire. At first, they were primarily Jewish in character but through the missionary work of St Paul, known later as the Apostle to the Gentiles, this new religion began to spread into the Greco-Roman world. By the Emperor’s reign, a tiny community of believers, led according to tradition by St. Peter, had established a religious beachhead in Rome itself. The problem the early Christians faced in Rome, though, was not just that their religion, in comparison to the wider pagan world, struck the average Roman as downright weird, but also that at this point most Christian adherents were non-citizen resident aliens in the city who spoke primarily Greek or Hebrew. So the Christians in Rome looked different, spoke a different language, usually came from the lower rungs of the social ladder, and belonged to a strange monotheistic cult that seemed to have cannibalistic overtones. All in all, they were capital O Other in every sense of the word. And as has been proven over and over again by history, whenever terrible things happen to a community – economic problems, floods, plagues, fires – it is the capital O Others who usually get blamed. So desperate to shift responsibility for the great fire away from himself, the Emperor looked at these Others and decided to lay it all on them.”

The only change I have made to this podcast text, recorded in August 2009, was my substitution of the central character’s title instead of his name. Even with that switch, there’s little surprise who that Emperor was.

Nero.